Spade company trial balance may 31 – The Spade Company Trial Balance as of May 31 provides a crucial snapshot of the company’s financial health. It serves as a foundation for financial statement preparation and plays a vital role in ensuring the accuracy and reliability of the financial reporting process.

This comprehensive guide delves into the intricacies of the trial balance, exploring its purpose, structure, and significance. We will analyze common errors and inconsistencies, discuss adjusting entries, and demonstrate the preparation of an adjusted trial balance. Furthermore, we will explore the process of financial statement preparation and uncover key insights revealed by the financial statements.

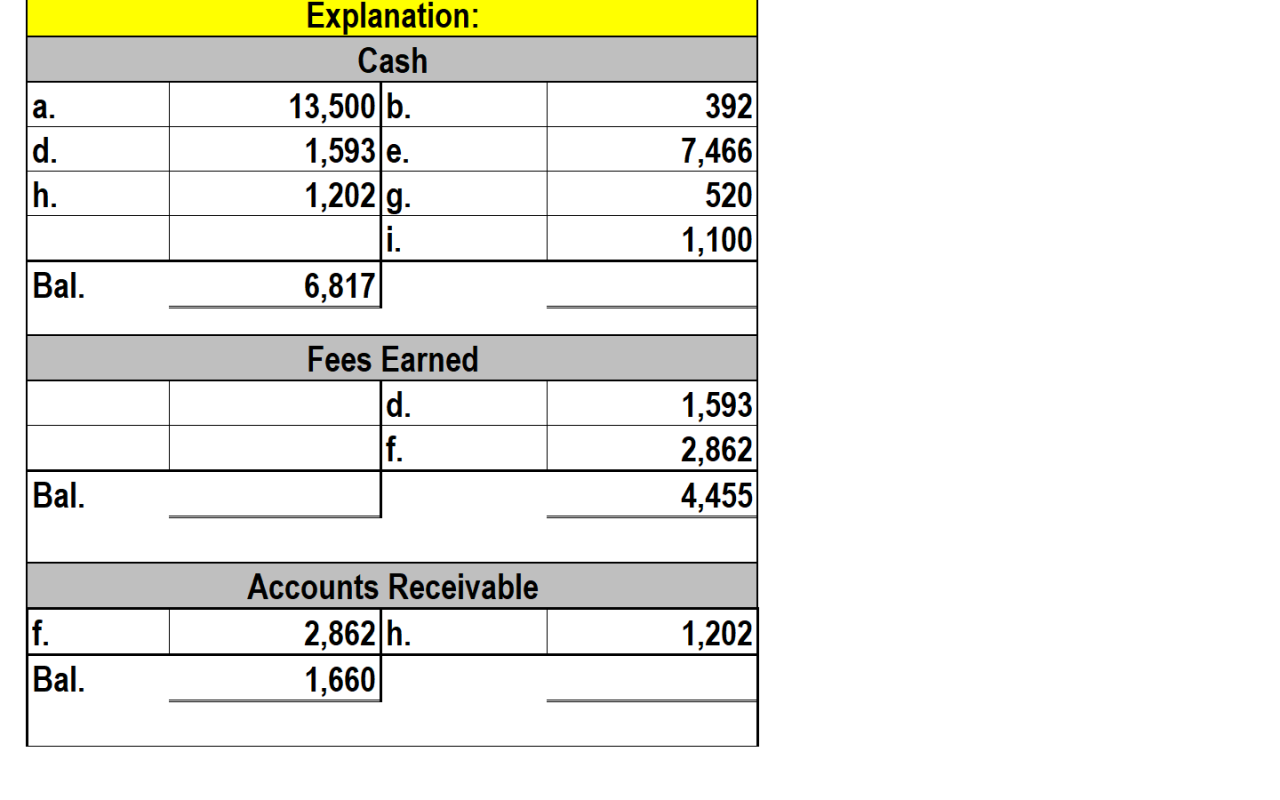

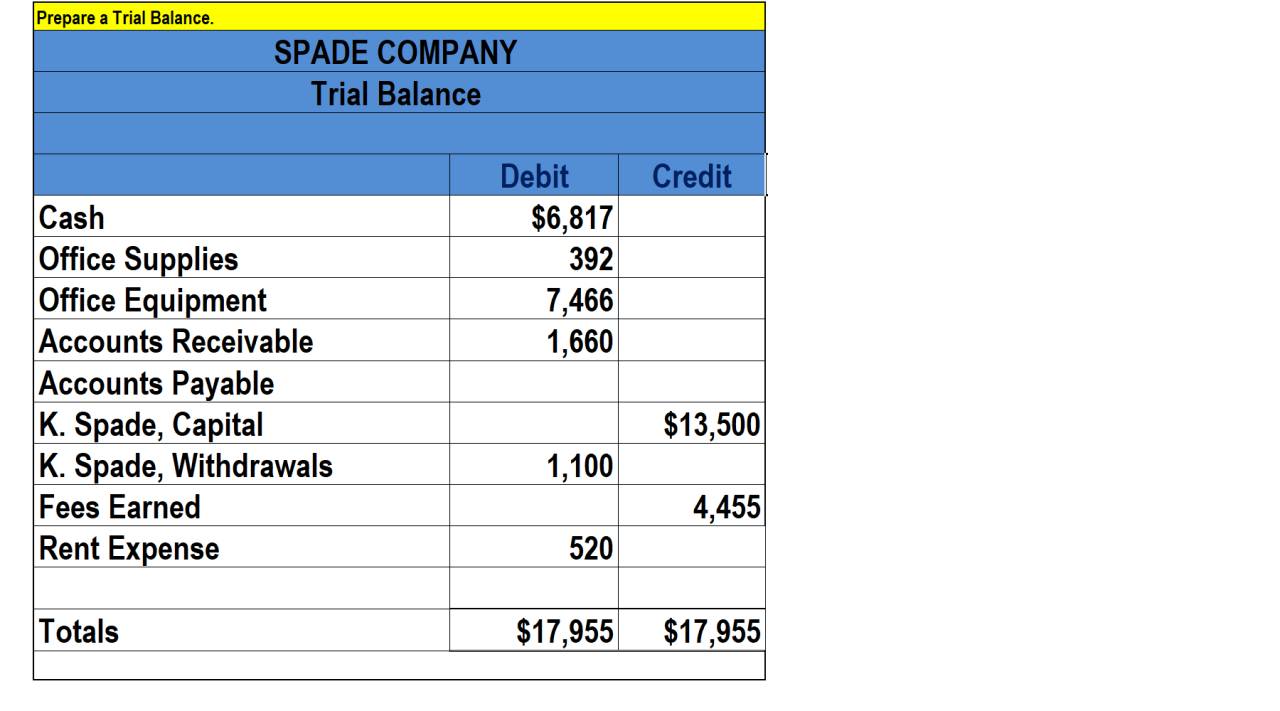

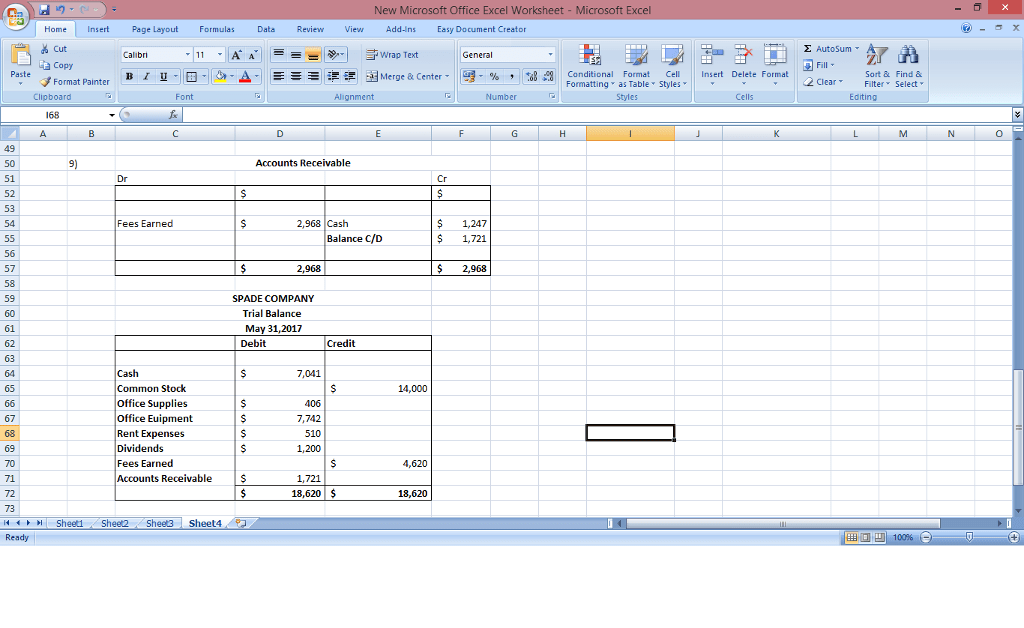

Spade Company Trial Balance as of May 31: Spade Company Trial Balance May 31

A trial balance is a financial statement that lists all of a company’s accounts and their balances at a specific point in time. It is used to check the accuracy of the accounting records and to ensure that the debits and credits are equal.

The trial balance is an important tool for financial analysis and is used by accountants, auditors, and other financial professionals.

The trial balance is typically prepared at the end of an accounting period, such as a month or a year. It is created by listing all of the company’s accounts in a vertical format, with the debit balances on the left side and the credit balances on the right side.

The total debits and credits should be equal, and if they are not, it indicates that there is an error in the accounting records.

Format and Structure of a Trial Balance

The format and structure of a trial balance can vary depending on the size and complexity of the company. However, the following information is typically included:

- Account Name: The name of the account, such as Cash, Accounts Receivable, or Inventory.

- Debit Balance: The total of all debit entries in the account.

- Credit Balance: The total of all credit entries in the account.

The trial balance is a valuable tool for financial analysis. It can be used to identify errors in the accounting records, to track the company’s financial performance, and to make informed decisions about the future.

Sample Trial Balance for Spade Company as of May 31

| Account Name | Debit Balance | Credit Balance |

|---|---|---|

| Cash | $10,000 | |

| Accounts Receivable | $20,000 | |

| Inventory | $30,000 | |

| Equipment | $40,000 | |

| Accounts Payable | $10,000 | |

| Notes Payable | $20,000 | |

| Owner’s Equity | $30,000 | |

| Revenues | $40,000 | |

| Expenses | $20,000 | |

| Totals | $100,000 | $100,000 |

As you can see from the sample trial balance, the total debits and credits are equal, which indicates that the accounting records are accurate. The trial balance can be used to track the company’s financial performance and to make informed decisions about the future.

Analysis of Trial Balance

A trial balance is a list of all the accounts in the general ledger with their debit and credit balances. It is used to check the accuracy of the accounting records and to make sure that the debits equal the credits.

Any errors or inconsistencies in the trial balance can indicate that there is a problem with the accounting records.

There are several potential causes of errors in a trial balance. These include:

- Mathematical errors

- Posting errors

- Omission errors

- Commission errors

Mathematical errors are simply mistakes in addition or subtraction. Posting errors occur when a transaction is posted to the wrong account or for the wrong amount. Omission errors occur when a transaction is not recorded at all. Commission errors occur when a transaction is recorded twice.

Errors in the trial balance can have a significant impact on the financial statements. For example, an error in the cash account can lead to an incorrect balance sheet. An error in the sales account can lead to an incorrect income statement.

Identifying Errors in the Trial Balance

There are several ways to identify errors in a trial balance. One way is to look for accounts with zero balances. Another way is to look for accounts with debit balances that do not have corresponding credit balances, or vice versa.

Once errors have been identified, they should be corrected. The best way to correct an error is to reverse the original transaction and then re-record it correctly.

Adjusting Entries

Adjusting entries are journal entries made at the end of an accounting period to update the balances of accounts to reflect their actual financial positions. These entries are necessary to ensure that the financial statements accurately represent the company’s financial performance and position.

The following adjusting entries need to be made as of May 31:

Depreciation Expense

Depreciation expense is an adjusting entry that allocates the cost of a capital asset over its useful life. The purpose of this entry is to recognize the expense associated with using the asset and to reduce the asset’s book value.

Accrued Interest Expense

Accrued interest expense is an adjusting entry that recognizes interest expense that has been incurred but not yet paid. The purpose of this entry is to match the expense with the period in which it was incurred.

Accrued Salaries Expense

Accrued salaries expense is an adjusting entry that recognizes salaries expense that has been incurred but not yet paid. The purpose of this entry is to match the expense with the period in which it was incurred.

Prepaid Insurance Expense

Prepaid insurance expense is an adjusting entry that allocates the cost of prepaid insurance over the period of coverage. The purpose of this entry is to recognize the expense associated with using the insurance and to reduce the asset’s book value.

The following table summarizes the adjusting entries:

| Account | Debit | Credit |

|---|---|---|

| Depreciation Expense | $xxx | Accumulated Depreciation |

| Interest Expense | $xxx | Interest Payable |

| Salaries Expense | $xxx | Salaries Payable |

| Insurance Expense | $xxx | Prepaid Insurance |

Adjusted Trial Balance

An adjusted trial balance is a financial statement that lists all of a company’s accounts and their balances after adjusting entries have been recorded. Adjusting entries are made at the end of an accounting period to ensure that the financial statements are accurate and up-to-date.

They are used to record transactions that have occurred but have not yet been recorded in the company’s accounting system.

The adjusted trial balance is used to prepare the company’s financial statements, including the income statement, balance sheet, and statement of cash flows. It is also used to identify any errors that may have been made in the recording of transactions.

Differences Between the Unadjusted and Adjusted Trial Balances

The unadjusted trial balance is a list of all of a company’s accounts and their balances before adjusting entries have been recorded. The adjusted trial balance is a list of all of a company’s accounts and their balances after adjusting entries have been recorded.

The following are the key differences between the unadjusted and adjusted trial balances:

- The unadjusted trial balance does not include any adjusting entries.

- The adjusted trial balance includes all of the adjusting entries.

- The unadjusted trial balance may not be accurate or up-to-date.

- The adjusted trial balance is accurate and up-to-date.

Significance of the Adjusted Trial Balance

The adjusted trial balance is a significant financial statement because it provides a snapshot of a company’s financial position at a specific point in time. It is used to prepare the company’s financial statements and to identify any errors that may have been made in the recording of transactions.

Financial Statement Preparation

The adjusted trial balance serves as the foundation for preparing financial statements, which provide a comprehensive overview of a company’s financial performance and position. The three primary financial statements are the income statement, balance sheet, and statement of cash flows.

Income Statement

The income statement summarizes a company’s revenues, expenses, and net income over a specific period, typically a quarter or a year. It shows how a company generates revenue, incurs expenses, and ultimately determines its profitability.

Revenues

List all revenue-generating activities, such as sales of goods or services.

Expenses

Categorize expenses based on their nature, such as cost of goods sold, operating expenses, and interest expenses.

Net Income

Calculate net income by deducting total expenses from total revenues.

Balance Sheet

The balance sheet provides a snapshot of a company’s financial position at a specific point in time. It shows the company’s assets, liabilities, and equity.

Assets

List all assets owned by the company, such as cash, accounts receivable, inventory, and property, plant, and equipment.

Liabilities

List all obligations owed by the company, such as accounts payable, notes payable, and long-term debt.

Equity

Calculate equity by subtracting total liabilities from total assets.

Statement of Cash Flows, Spade company trial balance may 31

The statement of cash flows tracks the movement of cash and cash equivalents within a company over a specific period. It shows how cash is generated and used in operating, investing, and financing activities.

Operating Activities

Summarize cash flows from core business operations, such as net income, depreciation, and changes in working capital.

Investing Activities

List cash flows related to investments, such as purchases and sales of property, plant, and equipment.

Financing Activities

Include cash flows from financing sources, such as issuance of stock, payment of dividends, and borrowing or repayment of loans.

Key Insights and Trends

Analyzing financial statements can reveal key insights and trends about a company’s financial performance and position. By comparing financial statements over time, investors and analysts can assess a company’s growth, profitability, liquidity, and solvency.

Growth

Track changes in revenue and expenses to identify trends in sales and profitability.

Profitability

Analyze net income and gross profit margins to evaluate a company’s ability to generate profits.

Liquidity

Assess a company’s ability to meet short-term obligations by examining its current ratio and quick ratio.

Solvency

Evaluate a company’s long-term financial health by analyzing its debt-to-equity ratio and times interest earned ratio.

Helpful Answers

What is the purpose of a trial balance?

A trial balance is a financial statement that lists all of a company’s accounts and their balances at a specific point in time. It is used to check the accuracy of the accounting records and to ensure that the total debits equal the total credits.

What are some common errors that can occur in a trial balance?

Some common errors that can occur in a trial balance include: – Incorrect account balances – Missing accounts – Transposition errors – Sign errors

What is the importance of an adjusted trial balance?

An adjusted trial balance is a trial balance that has been adjusted to reflect all of the adjusting entries that have been made at the end of an accounting period. It is used to prepare the financial statements.